When it comes to technology stocks in 2023, it seems like investors are hearing corporate executives emphasize two concepts in particular: artificial intelligence (AI) and profitability.

For example, after investing heavily in metaverse ambitions, Meta Platforms seemingly lost sight of its core advertising business and experienced shrinking revenue and profit. Subsequently, investors punished the stock, prompting Chief Executive Officer Mark Zuckerberg to declare 2023 as Meta's "year of efficiency." Moreover, both Alphabet and Microsoft have invested substantial sums into generative AI as each looks for a leg up in the area.

For Amazon (NASDAQ: AMZN), leadership has echoed themes similar to its FAANG cohorts. The last several quarters have been rough for the e-commerce giant as operating losses were beginning to mount. However, the company's second-quarter 2023 earnings report had several highlights and very few lowlights, if any.

Let's unpack the second-quarter report and make a case for why now is a great opportunity to buy the stock.

A treasure chest of hidden gems

Amazon is best known for its e-commerce marketplace and speedy delivery. But the graphic below does an exceptional job in breaking out all of Amazon's separate businesses.

It shows that the lion's share of Amazon's revenue is generated from online sales and third-party seller services, which is really just an extension of the company's marketplace. But when peeling back the onion, it becomes clear that Amazon is far more than an online shopping destination.

The company has built an extremely successful cloud computing business, Amazon Web Services (AWS), as well as a growing advertising segment. For the period ended June 30, AWS generated $22.1 billion in revenue, putting its annual run rate within striking distance of $100 billion. It looks inevitable that AWS will reach this milestone, which would make it Amazon's third business unit generating that much annual revenue.

For the quarter ended June 30, Amazon generated $10.7 billion from advertising revenue, for 22% growth year over year. By comparison, during the second quarter, Alphabet had 3% growth year over year from Google Advertising, while Meta's advertising revenue increased 12%.

Although an accelerating top line is encouraging to see, investors might want to know how much this growth is costing Amazon.

Image source: Company filings and The Motley Fool

Cash flow is king

The graphic above shows that each category of Amazon's expenses increased during the second quarter. Nonetheless, the company turned a profit of $6.8 billion compared to a loss of $2 billion in the same period last year.

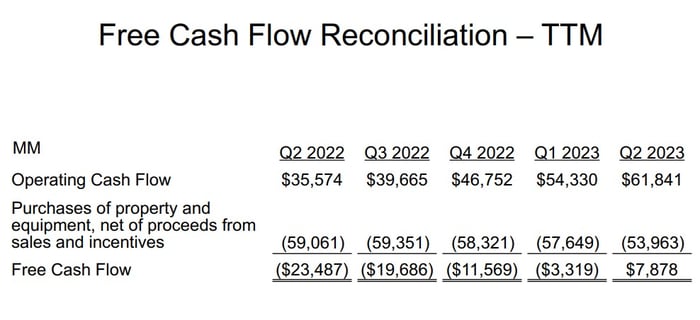

When analyzing profitability, I prefer to look beyond net income. The chart below comes directly from Amazon's second-quarter 2023 investor presentation, and I think it serves as a real testament to how far the company has come over the last year. For the 12-month period ended June 30, its free cash flow was $7.9 billion, as the table below shows.

Image source: Amazon's Q2 2023 investor presentation

Bottom line

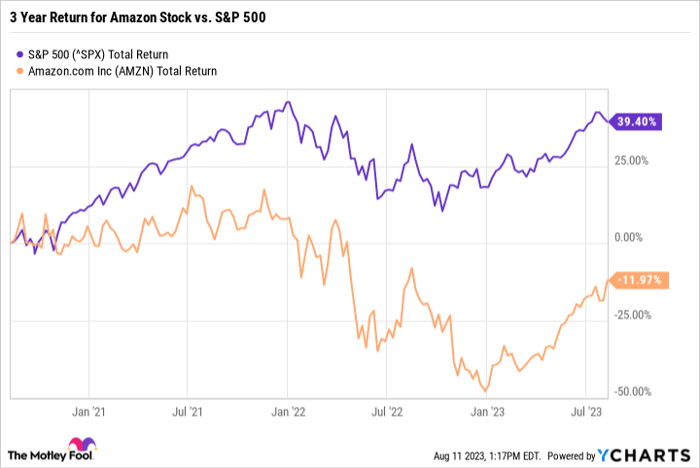

The stock chart below can be sobering to look at. Over the past three years, Amazon stock has drastically underperformed the S&P 500. Given how well the stock performed during the market euphoria in 2020, this is almost hard to believe. But the chart is a reminder that stocks can go down just as quickly as they go up.

Data source: YCharts.

While the broader economy remains an enigma, Amazon's earnings can shed light on a few things. Despite lingering inflation, consumers appear to still be spending online. Moreover, while companies of all sizes resorted to layoffs and other cost-cutting throughout the first half of the year, spending on digitial transformation tools such as cloud applications continues.

The stock currently trades at a price-to-sales (P/S) ratio of 2.6, relatively unchanged over the past year. This is intriguing given the company's return to positive free cash flow and accelerating sales across core businesses.

Amazon's latest quarter went a long way in my book. While I understand that one quarter, good or bad, is not indicative of the future, I feel comfortable that the long-term picture looks strong. I believe that AWS and advertising will continue to blossom, while e-commerce is a steady nucleus to Amazon's diversified portfolio of businesses.

Although the stock is up more than 60% so far in 2023, the company's current valuation has me believing that there is more room for it to climb.

10 stocks we like better than Amazon.com

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Amazon.com wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of August 1, 2023

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Adam Spatacco has positions in Alphabet, Amazon.com, Meta Platforms, and Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon.com, Meta Platforms, and Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

0 Comments